Embedded Payments Guide: Your Roadmap to Success in 2026

Digital commerce is evolving at lightning speed in 2026, and the rise of embedded payments is at the heart of this transformation. Businesses that ignore this shift risk falling behind as seamless, integrated payment experiences become the new standard.

This guide is your roadmap to mastering embedded payments. Whether you’re a business leader aiming for growth or a developer building the next big thing, you’ll find strategies, insights, and practical frameworks to help you thrive.

Discover what embedded payments are, why they matter, and how leading platforms are leveraging them for a competitive edge. We’ll dive into trends, technology choices, compliance essentials, and step-by-step implementation.

Ready to unlock new revenue streams and future-proof your business? Let’s explore the future of digital transactions together.

Understanding Embedded Payments in 2026

Embedded payments are transforming how we interact with digital platforms in 2026. Unlike traditional payment gateways that redirect users to external sites, embedded payments are built directly into the platform’s workflow. Whether you are hailing a ride, subscribing to a SaaS tool, or buying from an online store, payment happens seamlessly within the app. APIs (Application Programming Interfaces) and SDKs (Software Development Kits) power this experience, letting businesses own the payment journey end to end. Curious about the technical details and how embedded payments differ from legacy processors? Embedding Payments Explained offers an in-depth look at the architecture and real-world use cases.

What Are Embedded Payments?

At their core, embedded payments are financial transactions processed directly within a digital platform’s environment. Unlike external gateways that interrupt the customer journey, embedded payments keep users engaged from start to finish. APIs and SDKs connect platforms to payment networks, banks, and even crypto wallets, allowing for customization and control. For example, ride-sharing apps let users pay and tip drivers in-app without leaving the interface. E-commerce platforms like Shopify and SaaS products increasingly use embedded payments to simplify recurring billing or split payouts. This approach reduces friction, speeds up checkouts, and fosters trust by making payments almost invisible to the user.

Market Growth and Trends

The embedded payments market is experiencing explosive growth in 2026. According to industry research, the global embedded finance sector is projected to reach $138 billion by this year, as vertical SaaS and platform-based commerce continue to rise. Retail, transportation, and B2B marketplaces are leading adoption, driven by demand for integrated experiences. Open banking initiatives and the deployment of real-time payment rails are accelerating innovation, allowing instant settlements and broader access to financial services. The table below illustrates recent market data and adoption trends:

| Year | Global Market Size (USD) | Leading Industries |

|---|---|---|

| 2024 | $85 billion | Retail, Transport |

| 2026 | $138 billion | SaaS, B2B Platforms |

The future points toward even deeper integration as regulations support data sharing and interoperability.

Key Benefits for Businesses and Users

Businesses adopting embedded payments unlock significant advantages:

- Enhanced customer retention and higher lifetime value

- Streamlined checkout, leading to increased conversion rates

- New revenue streams through value-added services like subscriptions or instant payouts

- Lower costs by reducing reliance on third-party processors and automating back-office tasks

For instance, Shopify’s embedded payments have enabled merchants to boost sales and simplify global expansion. Users benefit from one-click checkouts, transparent fees, and payment methods tailored to their preferences. The end result is a smoother, more trustworthy transaction process that builds loyalty and drives growth.

Challenges and Considerations

Despite the promise, embedded payments come with their own set of challenges. Technical complexity can slow integration, especially for platforms with legacy systems. Security is non-negotiable, as businesses must guard against fraud, data breaches, and evolving threats. Compliance with local and international regulations like PSD2 and GDPR requires constant vigilance and expertise. Building user trust is critical, particularly during onboarding and consent flows. Finally, companies must strike a balance between customization for a unique experience and scalability for growth.

The Embedded Payments Ecosystem: Players, Technologies & Partnerships

The embedded payments ecosystem in 2026 is a dynamic network of technologies, business models, and partnerships that power seamless digital transactions. Understanding how these components interact is essential for any business aiming to leverage embedded payments for growth and innovation.

Core Components and Architecture

At the heart of embedded payments are robust technical building blocks that enable smooth payment experiences. APIs (Application Programming Interfaces) and SDKs (Software Development Kits) allow platforms to connect payment services directly into their products.

A typical architecture includes:

- Payment orchestration layers to manage routing and optimize transaction processing.

- Payment facilitators (PayFacs) who simplify merchant onboarding and compliance.

- Merchant of record models where platforms handle payments on behalf of sellers.

- Banking-as-a-service (BaaS) providers offering modular financial services like accounts, cards, and KYC.

These components work together to create a frictionless payment environment. By embedding payments, platforms eliminate the need for users to leave their ecosystem, streamlining checkout and increasing engagement.

Key Stakeholders and Roles

The embedded payments landscape brings together a diverse group of stakeholders. Each plays a unique part in ensuring smooth, secure, and compliant transactions.

| Stakeholder | Role in Embedded Payments |

|---|---|

| Merchants | Offer goods/services, initiate payments |

| Platforms | Integrate payment flows, manage user journeys |

| Developers | Build and maintain integrations |

| End-users | Make purchases, receive payouts |

| Payment processors | Handle transaction routing and settlement |

| Acquirers and Banks | Provide accounts, manage funds |

| Fintechs | Enable infrastructure and innovation |

Collaboration among these players is crucial. Developers translate business needs into technical solutions, while fintechs and banks provide the backbone for secure, compliant payments.

Technology Trends Driving Embedded Payments

Cutting-edge technology is transforming how embedded payments function. Real-time payments (RTP) and instant settlement are becoming standard, reducing delays and improving liquidity for businesses.

Security remains paramount. Tokenization and strong encryption protect sensitive data, while advanced fraud detection systems use AI and machine learning for real-time risk scoring. For example, a platform might use behavioral analytics to flag suspicious transactions instantly.

Payment APIs now support a wide range of payment methods, including digital wallets and even crypto. This flexibility is crucial for platforms serving global and diverse user bases.

Strategic Partnerships and Ecosystem Collaboration

No single company can deliver the full potential of embedded payments alone. Strategic partnerships between fintechs, banks, and digital platforms are driving innovation at scale.

Industry leaders like Stripe Connect, Adyen for Platforms, and Plaid are frequently chosen for their robust APIs and global reach. Co-innovation is common, with shared compliance responsibilities and technical support ensuring secure, reliable integrations.

For a deeper perspective on how collaboration is transforming business models, Embedded Payments as a Growth Engine offers expert insights into the shift from utility to strategic value in the embedded payments space.

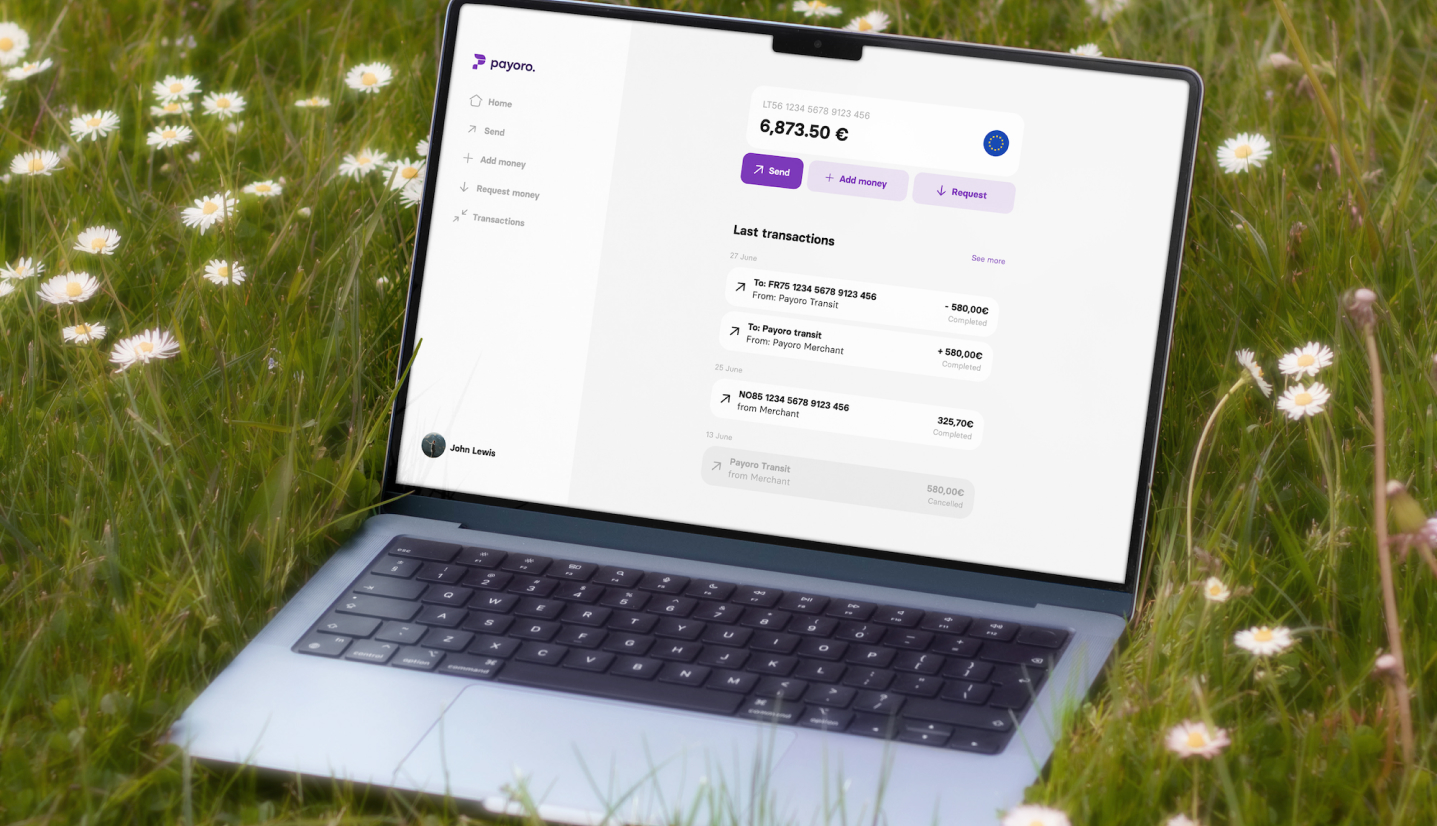

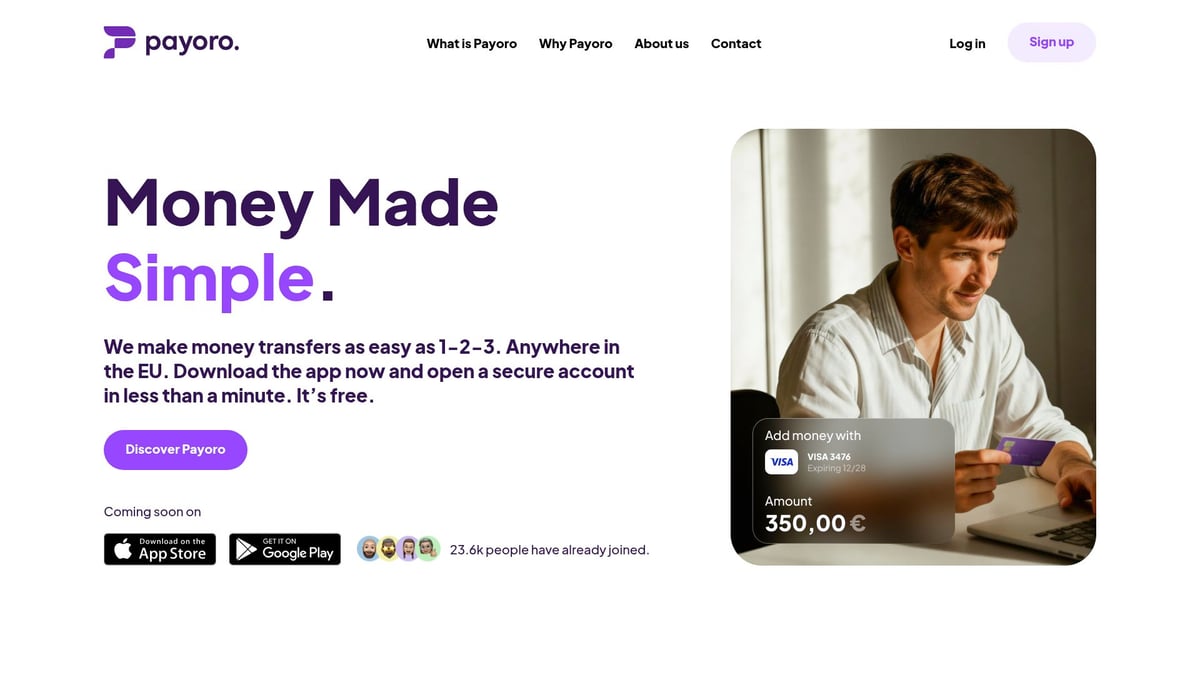

Payoro: Seamless Embedded Payment Integration

Payoro stands out with its API-driven embedded payments solutions, offering real-time, secure transactions across the EU. Merchants benefit from unified fiat and crypto support, rapid onboarding, and highly customizable features.

Businesses use Payoro to enable embedded cross-border payouts, reducing settlement times and operational complexity. With Payoro, integrating embedded payments becomes a streamlined, future-ready process.

Step-by-Step Roadmap: How to Implement Embedded Payments in 2026

Implementing embedded payments in 2026 requires a clear, pragmatic approach. Whether you’re a platform, SaaS provider, or digital marketplace, following a structured roadmap can help you maximize value, reduce risk, and deliver seamless experiences that set you apart.

Assessing Business Needs and Readiness

Start by mapping your current payment flows and identifying friction points. Where do customers drop off? Are manual processes slowing you down? Engage teams across product, finance, and engineering to get a holistic view.

Outline your goals for embedded payments. Is it about reducing fees, accelerating payouts, or improving customer retention? Create a customer journey map to visualize where payments are embedded and where improvements are possible.

Assess technical readiness. Do you have in-house development resources? Are your current systems API-friendly? Align stakeholders early and secure buy-in for the investment required to transform your payment infrastructure with embedded payments.

Selecting the Right Embedded Payments Partner

Choosing a partner is a pivotal decision. Evaluate candidates based on integration ease, compliance expertise, support responsiveness, and scalability for your future growth.

Compare providers by reviewing costs, supported payment methods, and real-world case studies. Look for a platform offering sandbox environments and robust developer documentation.

Prioritize partners with a proven track record in your industry. Consider additional factors such as uptime guarantees and dispute management capabilities. The right embedded payments partner will not only solve today’s challenges but also support your long-term ambitions.

Designing User Experience and Payment Flows

Great embedded payments experiences start with intuitive design. Minimize steps in checkout and optimize for mobile-first interactions. Use embedded checkout widgets, recurring billing modules, or split payment features to fit your business model.

Don’t overlook accessibility—ensure your payment flows are usable for everyone. Localize payment methods and interfaces for different regions, currencies, and languages.

Test with real users to uncover friction. Iterate on feedback to create a seamless, branded payment journey that feels native to your platform. Embedded payments should blend into the user experience, not disrupt it.

Technical Integration and API Implementation

Technical integration is where plans become reality. Review API documentation carefully and plan your implementation in phases. Use tokenization to secure sensitive data, and ensure adherence to PCI DSS standards.

Set up robust error handling and test for edge cases such as network failures or declined transactions. Use sandbox environments for safe, iterative development.

Security is paramount. Incorporate best practices for payment security, such as those detailed in Embedded Payments Implementation Best Practices. Validate transaction reliability before going live to ensure embedded payments are both safe and resilient.

Compliance, Risk, and Fraud Management

Navigating compliance is a continuous process. Stay current with PSD2, GDPR, and local AML/KYC laws. Implement real-time fraud monitoring to spot anomalies and prevent attacks.

Design user onboarding flows that collect necessary consents and documents. Automate chargeback management and dispute resolution where possible.

Build trust by making compliance visible. Communicate your security measures and privacy policies to users. Embedded payments success depends on both technical and regulatory diligence.

Go-Live, Monitoring, and Optimization

Roll out embedded payments in phases, starting with a subset of users. Monitor key metrics like conversion rates, payment failures, and downtime.

Leverage A/B testing to optimize checkout flows and payment methods. Use analytics dashboards to track trends and identify bottlenecks.

Gather feedback from users and merchants. Iterate quickly to address pain points and enhance the embedded payments experience. Continuous improvement is essential for staying competitive.

Scaling and Expanding Embedded Payments

Once launched, plan for growth. Support multiple currencies and expand to new countries as your business evolves.

Add new payment methods and value-added services, such as automated invoicing or instant payouts, to meet changing customer needs. Prepare your infrastructure for increased transaction volumes by investing in scalable, cloud-native technology.

Staying agile ensures your embedded payments solution can adapt to new markets, regulations, and opportunities as they emerge.

Navigating Compliance, Security, and Regulation

Compliance, security, and regulation form the backbone of any robust embedded payments strategy. As the market matures in 2026, businesses must navigate a complex and evolving landscape to ensure trust, efficiency, and long-term growth.

Regulatory Landscape in 2026

Embedded payments are reshaping the financial ecosystem, but regulatory oversight is intensifying. In the EU, PSD2 (Payment Services Directive 2) and Strong Customer Authentication (SCA) remain central, requiring rigorous authentication and open banking APIs. The UK continues to adapt post-Brexit, aligning with both EU standards and its own Financial Conduct Authority (FCA) requirements.

In the US, regulations vary by state, but federal agencies focus on anti-money laundering (AML) and know-your-customer (KYC) mandates. Platforms looking to offer embedded payments must secure appropriate licensing, such as becoming a registered payment facilitator or partnering with a licensed entity.

A quick comparison helps clarify the major regulatory touchpoints:

| Region | Core Regulation | Key Focus | Licensing Needed? |

|---|---|---|---|

| EU | PSD2, SCA | Open banking, SCA | Yes |

| UK | FCA, PSD2 | AML, SCA | Yes |

| US | State/Federal | AML, KYC | Often, varies by use |

Staying ahead of these requirements is critical for embedded payments providers and platforms to maintain customer trust and avoid costly penalties.

Data Security and Privacy Essentials

With embedded payments, data security is non-negotiable. PCI DSS (Payment Card Industry Data Security Standard) compliance is mandatory for any business handling cardholder data. This means encrypting sensitive information at rest and in transit, using secure APIs, and conducting regular vulnerability scans.

Tokenization is a best practice for protecting payment data. Instead of storing card details, the system replaces them with a unique token, reducing exposure in case of a breach. For example:

def tokenize_card(card_number):

# Replace card number with a secure token

return hashlib.sha256(card_number.encode()).hexdigest()

GDPR and ePrivacy regulations add another layer, requiring explicit user consent for data processing and clear data retention policies. Embedded payments solutions must make privacy a visible feature, not just a backend process.

Fraud Prevention and Risk Management

Fraudsters target embedded payments platforms due to the high transaction volume and valuable data. Advanced machine learning models now power real-time fraud detection, flagging suspicious behaviors like rapid-fire transactions or unusual login locations.

Behavioral analytics help build user profiles, allowing systems to spot deviations quickly. For instance, if a user suddenly initiates large cross-border payouts, the platform can trigger step-up authentication or manual review.

Regular monitoring and tight integration with payment processors reduce the risk of chargebacks and unauthorized transactions. Embedded payments providers must continually refine their risk models, learning from new fraud patterns as they emerge.

Handling Disputes, Chargebacks, and Refunds

A seamless embedded payments experience includes efficient dispute resolution. Automated workflows can route chargeback cases to the right team, ensuring compliance with regulatory timelines. Some platforms use dashboards to track dispute status, from initial claim to resolution.

Chargeback mitigation strategies include clear transaction descriptors, proactive communication, and robust documentation. Keeping users informed during the process builds trust and can reduce repeat disputes.

Regulations often specify response windows, so it’s vital to have systems in place that flag deadlines and automate reminders. Embedded payments platforms that streamline refunds and disputes create a competitive advantage through superior user experience.

Cross-Border Payments and Multi-Currency Compliance

Expanding embedded payments across borders introduces new regulatory hurdles. Platforms must manage foreign exchange (FX), adhere to local AML and KYC laws, and support multiple currencies. Each country may have its own reporting and settlement requirements, making compliance a moving target.

For a deeper dive on integrating cross-border capabilities into embedded payments, explore this guide to Cross-Border Payment Integration. A well-architected solution can unlock global markets, but only if compliance keeps pace with innovation.

Future-Proofing Your Embedded Payments Strategy

Staying ahead with embedded payments in 2026 means looking beyond today’s solutions. New technologies, changing user demands, and evolving regulations are reshaping what’s possible. To secure your place in this fast-moving landscape, you need to anticipate what’s next and adapt with agility.

Innovations on the Horizon

Emerging technologies are expanding the boundaries of embedded payments. Blockchain and decentralized finance (DeFi) are enabling programmable payments and transparent transaction flows. Digital wallets are rapidly gaining traction, and super apps are integrating payments, messaging, and financial services into one smooth interface.

For example, platforms like Payoro’s SuperApp are redefining how businesses and consumers interact with financial services, offering everything from instant account creation to embedded lending. Embedded payments now support not only fiat but also digital assets, giving users more flexibility and control. Expect programmable payments—automated, rules-based transfers—to become mainstream, driving new business models and service offerings.

Adapting to Changing Customer Expectations

Customer expectations are evolving quickly. Instant payments, seamless onboarding, and personalized experiences are no longer optional—they are standard. Embedded payments play a critical role in meeting these demands by supporting real-time payouts and frictionless checkout flows.

Platforms need to integrate loyalty programs and tailored offers directly into payment experiences. For instance, subscription platforms now use embedded payments to offer instant upgrades or one-click renewals, boosting both retention and satisfaction. The ability to localize payment options and support multiple currencies is also crucial for reaching global customers.

Leveraging Data and Analytics

With embedded payments, every transaction generates rich data that can fuel business intelligence. Companies are using predictive analytics to understand customer behavior, reduce churn, and optimize pricing. Privacy-first approaches, such as anonymizing user data, ensure compliance while still allowing for actionable insights.

Automated billing and reconciliation are now standard, freeing teams from manual processes and reducing errors. Leveraging solutions like Automated Billing Solutions can streamline operations, improve transparency, and offer customers more flexible payment options. Harnessing data from embedded payments enables businesses to uncover new revenue streams and deliver more targeted experiences.

Building for Scalability and Resilience

Scaling embedded payments requires a robust, cloud-native infrastructure. High availability and redundancy are essential to minimize downtime and ensure consistent service. Disaster recovery plans must be in place to handle unexpected events, from cyberattacks to regulatory changes.

Preparing for market shifts means designing flexible systems that adapt to new payment methods, currencies, and compliance requirements. Platforms should prioritize modular architectures, allowing for rapid updates and integration of emerging technologies. This resilience protects both revenue and reputation as the ecosystem evolves.

Creating Competitive Advantage with Embedded Payments

The most successful platforms use embedded payments as a strategic differentiator. By offering unique payment experiences—such as instant supplier payouts or integrated loyalty rewards—businesses can stand out in crowded markets. Monetizing payments, for example through value-added services or premium support, opens new revenue opportunities.

Consider a SaaS provider that increased customer retention by embedding payments directly into its platform, reducing churn and enabling upsell of automated billing features. The key is to continually refine your approach, leveraging best practices and industry benchmarks to stay ahead. In 2026, embedded payments are not just a feature—they are a foundation for long-term growth and innovation.

Real-World Success Stories and Lessons Learned

Real-world examples provide vital insight into the tangible impact of embedded payments. Success stories, platform innovations, and even failed attempts all reveal what works and what to avoid. By examining these lessons, businesses can shape their own embedded payments strategies for 2026 and beyond.

Case Study: E-Commerce Platform Transformation

An e-commerce platform’s journey with embedded payments shows the technology’s power to drive growth. Previously, customers faced a multi-step checkout process leading to frequent cart abandonment. After integrating embedded payments directly into the platform, the checkout became a single, frictionless step.

The result was a significant uplift in conversion rates and customer satisfaction. Merchants also gained access to richer transaction data, which enabled them to refine marketing and inventory strategies. The platform reported a measurable reduction in operational costs, as automation replaced manual payment reconciliation. This case highlights how embedded payments can be a catalyst for both revenue growth and improved user experience.

Fintech and B2B Platform Examples

Fintech and B2B marketplaces have embraced embedded payments to solve industry-specific challenges. For example, B2B platforms that once struggled with slow supplier payouts now offer instant settlements, improving cash flow and trust among participants.

Subscription management tools have also integrated embedded payments, automating invoicing and recurring billing. This shift has drastically reduced late payments and manual intervention. A leading illustration is the Payoro SuperApp Overview, which demonstrates how unified embedded payments can streamline onboarding, multi-currency support, and real-time cross-border payouts for platforms serving a diverse user base.

Lessons from Failed Implementations

Not every embedded payments rollout is a success. Common pitfalls often include:

- Underestimating regulatory complexity, resulting in costly delays.

- Neglecting user experience, which leads to poor adoption.

- Inadequate testing of edge cases, causing transaction failures at scale.

One company attempted to launch embedded payments without a phased rollout, leading to unexpected downtime and lost revenue. Another overlooked the importance of ongoing compliance monitoring, which exposed them to penalties. These stories reinforce the importance of planning, testing, and compliance vigilance for any embedded payments initiative.

Key Takeaways for 2026 and Beyond

Drawing on both wins and setbacks, several lessons emerge for businesses in 2026. Here is a practical checklist:

| Action Item | Why It Matters |

|---|---|

| Streamline user journeys | Boosts conversion and loyalty |

| Prioritize compliance | Reduces risk and builds trust |

| Invest in automation | Cuts costs and increases efficiency |

| Monitor market trends | Keeps your strategy future-proof |

Industry data confirms that embedded payments market growth is accelerating, and platforms that adapt quickly are best positioned for success. By learning from real-world examples and staying agile, organizations can unlock the full value of embedded payments in the years ahead.

You’ve seen how embedded payments are transforming digital commerce and how the right strategy can set you apart in 2026. If you’re ready to streamline your payment flows, unlock new revenue, and deliver seamless experiences for your customers, let’s take the next step together. Payoro’s secure, API-driven platform makes it easy to integrate real-time fiat and crypto payments into your business, no matter where you operate in the EU.

Curious about how embedded payments can work for you or want tailored advice for your business? Contact sales and start your journey toward payment innovation today.

Share article on

Related articles

See all articles iGaming Payout Solutions: How Operators Can Process Player Withdrawals Faster

iGaming operators lose players to slow withdrawals. Learn how modern payout solutions, from SEPA Instant to stablecoin settlement,...

KYC AML Compliance for Payouts: What Every Platform Needs to Know

Learn how KYC and AML compliance requirements apply to payout platforms in the EU. Practical framework for tiered...

Vendor Payouts: How Platforms Can Pay Suppliers Faster and Cheaper

Vendor payouts are slow and expensive for most platforms. Learn how to automate vendor payments, cut cross-border costs,...

Payment Orchestration Explained: Why Platforms Are Ditching Single-Provider Setups

Running payments through a single provider is a single point of failure. Payment orchestration gives platforms the routing,...